When Jeff, a retired marketing consultant from Chicago, was closing on his home sale, he received a new set of instructions at the last minute on where to send several thousand dollars in closing expenses. At first blush, the email looked legit with an official-looking logo and professional language specifying the amount owed and itemized expenses. But one thing caught his eye: The email address looked strange. Just to be safe, he called his mortgage broker.

“Don’t do that!” his broker told him in an alarmed voice. It was a scam. If he hit “send,” his closing fees would go to a thief who had been monitoring his emails. “I was a keystroke away from losing thousands of dollars,” Jeff recalled.

As the housing market sizzles across the country – with nearly 6 million homes bought last year – scammers have been finding new ways to tap into this once-secure market. Real estate transactions still demand reams of paperwork and regulations involving lawyers, brokers, title insurance companies and banks, but the fact that much of this work now takes place online gives thieves countless opportunities to exploit vulnerable buyers. Last year, more than 11,000 homeowners were scammed out of more than $220 million in closing funds alone, according to the American Land and Title Association, a trade group that represents professionals who perform property transactions.

Closing-fund theft is one of many real estate scams that have emerged and proliferated over the past two years or so. The main lure is to get people to send money to fake addresses. They include:

- Fake Rentals. Scamsters post rental ads – either for real properties they don’t own or “spoofs” they have created with photographs – on major sites like Craigslist. Typically they ask for below-market rates, get interested parties to put down a deposit, then disappear.

- Fraudulent Foreclosure Relief. Pioneered during the housing market crash in 2007-2009, this scam involves thieves promising a service that would end foreclosure proceedings. Thieves collect a fee of several hundred dollars, then disappear with the money.

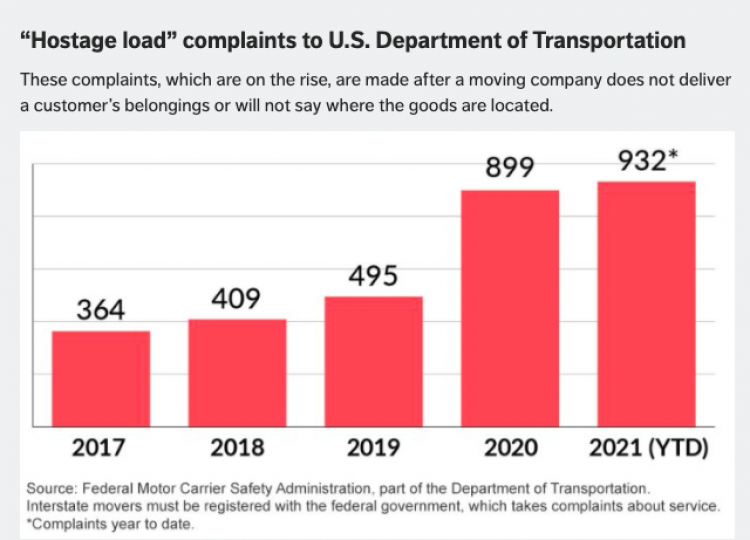

- Moving Scams. Most people don’t actually meet their movers before they hire them, which enables fraudulent operators to either take an upfront fee and not move clients’ possessions or hold furniture “hostage,” demanding a higher fee and refusing to complete the move unless they are paid more. Usually these bogus movers are pitched through moving “brokers.”

The pandemic has helped fuel the boom in real estate scams. More people working from home translates into more valuable information being sent over less secure personal Internet connections lacking firewall and other protections that offices might provide. The housing boom fueled by COVID – which has sparked demand but constrained new construction – has led to greater competition in many markets, leading increasing numbers of buyers to purchase homes sight unseen. The real estate company Redfin reports that 63% of homebuyers last year made an offer on a property they hadn’t seen in person. In addition, the rise of cryptocurrency makes it harder to trace bogus transactions and easier to launder ill-gotten gains.

The rise in real estate scams is part of a larger increase in crimes involving emailed funds. According to the Internet Crime Complaint Center (IC3), in 2020 the agency received 19,369 “Business Email Compromise (BEC)/ Email Account Compromise (EAC)” complaints with adjusted losses of more than $1.8 billion.

Scammers prey upon victims with a number of deception tools. They use “phishing” emails to mine valuable personal or financial information, claiming to falsely “verify” bank account or Social Security information. Or they may “spoof’ consumers into thinking that an email, text or call is from a real financial company, online retailer or the IRS.

Many of these scams originate overseas, yet because the perpetrators can create and shut down fake emails and websites quickly before regulators catch up with them, they are hard to trace and catch.

The Treasury Department, FBI and its Internet Crime Complaint Center broadly categorize closing-expense fraud under what they call “business email compromise.” The scam is relatively simple: A fake email pops up for a homeowner closing on a mortgage – usually on the day all the documents and closing expenses need to be verified and transferred. The false email lures the closing party into electronically transferring funds to a thief, who is hard to trace.

No. 7 in the FBI Cyberscam Top 10

The National Association of Realtors, the main trade association for the real estate industry, estimates that there were more than 13,000 complaints relating to property-related fraud last year, although that number includes rental fraud. Nevertheless, that puts real-estate email fraud in the top-10 list (No. 7) of the FBI’s most prevalent cyberscams.

Deanne Rymarowicz, associate counsel for the NAR, told RealClearInvestigations that cyberthieves have become diligent in stalking potential victims. “They look for pending sales in public records,” she said, “create profiles from their social media then hack or spoof their emails with false addresses.”

One positive statistic Rymarowicz discovered: When these thefts are reported to law enforcement agencies such as the FBI within 24 hours, “there is an 82% recovery rate of stolen funds. So acting quickly is important.”

Most people, however, are highly embarrassed when they are stung by these scams. As a result, only about 15% report them to authorities, according to the FBI.

Another industry group, the National Credit Union Association, stated that while these kinds of scams are increasing, what makes them “so enticing to criminals and easy to pull off is the nature of the real estate closing process, which is often hurried, and the fact that email is a commonly used method for providing legitimate instructions for sending funds at closing.” A spokesman for the group declined to comment further.

Other kinds of residential real estate fraud are more difficult to perpetrate, but involve slightly different modus operandi. As outlined in a piece RCI published last year, a notable rise in home title cybertheft was being observed by regulators. Although more sophisticated than closing-expense theft, these scams involved fraudulent home title transfers. Plain-vanilla mortgage fraud, involving fake financings, was rampant in the years following the credit meltdown of 2008. Thieves advertised “mortgage relief” scams and other ways to steal funds and personal information. Most of the swindles involved collecting upfront fees for fake mortgage services.

The newest wrinkle is that the cyberthief may “wash” the stolen funds into a cryptocurrency, which will make the transaction even harder to track if they use “tumbler” software that scrambles the route the transfer takes. “In 2020, the IC3 observed an increase in the number of complaints related to the use of identity theft and funds being converted to cryptocurrency,” the agency reported. When transferred into a digital currency, special software can cloak the transaction and hide the funds.

Earlier this year, the FBI also issued a statement on how crypto theft works: “The victim entity will receive a spoofed or otherwise compromised email that contains doctored wire instructions provided by the bad actor; however, since the requested transfer is directed to a traditional financial institution (where the cryptocurrency exchange has a custodial account), it is not easily identified by the victim.”

In response to the rapid explosion of these real estate scams in recent years, principal financial regulators and trade associations are seeing and have issued myriad consumer warnings in what they characterize as an epidemic of online fraud.

“Some [thieves] are stealing through phishing emails, some are monitoring social media who tend to announce things like closings,” said Mitria Wilson-Spotser, director of housing policy for the Consumer Federation of America. “An innocent act has become a calling card for thieves.”

The real estate industry; the Consumer Financial Protection Bureau, which also declined to comment beyond its website statement; and other government consumer protection agencies, have been proactive in telling consumers how to avoid these scams, which may continue to rise as more people do electronic transactions and don’t take time to sweat important details or use two-factor authentication.

Compounding the difficulty that regulators have in cracking down on these crimes is that real estate transactions are monitored by various jurisdictions and agencies, including multiple state and federal banking and law enforcement authorities, while data security and privacy concerns are often overseen by separate government divisions or agencies. The CFA’s Wilson-Spotser notes that “efforts to combat these scams fall under an incredibly leaky federal data security and privacy umbrella, which the CFPB doesn’t have jurisdiction over.”

While multiple eyes on these transactions can be a good thing, it’s difficult to know which agency to turn to if you’re scammed. Generally, banks, mortgage brokers and real estate agents have the biggest incentive to be the most aggressive watchdogs. But wire fraud involving financial transactions also comes under the umbrella of the Financial Crimes Enforcement Network, or FinCEN, the obscure sub-agency working with the Treasury and Justice departments. A FinCEN spokesperson noted that when authorities receive a closing-fund theft complaint, “we move quickly to track and make contact with foreign jurisdictions to assist in recovering the funds.”

Neither FinCEN nor the FBI would provide further details on how they handle enforcement.

The simplest safeguard in nearly every case, many experts told RCI, is to simply pick up the phone to confirm closing instructions with the official person assigned to the transaction details, who is usually a legitimate employee of a title company, bank or a lawyer. As Jeff in Chicago found out in the nick of time, if something smells fishy, it probably is. Instead of hitting “send” call you broker or bank.

This and all other original articles created by RealClearInvestigations may be republished for free with attribution. (These terms do not apply to outside articles linked on the site.)

We provide our stories for free but they are expensive to produce. Help us continue to publish distinctive journalism by making a contribution today to RealClearInvestigations.

Support RealClearInvestigations →